Many expats land in Asia-Pacific with a travel insurance policy, a sense of adventure, and a dangerous assumption: that they’re covered. They’re not. Travel insurance is built for short trips, not for the realities of living and working abroad for months or years at a time. A single hospitalisation in Singapore or a cancer diagnosis in Hong Kong can generate bills that run into the hundreds of thousands of dollars. This guide cuts through the noise, explains exactly what dedicated expat health insurance covers, and gives you a practical framework for choosing the right policy before you need it.

Table of Contents

- Why expats need dedicated health insurance

- Understanding your options: Expat health insurance plans in Asia-Pacific

- Key factors affecting costs and coverage

- How to compare and choose the best provider

- A fresh take: What most expats miss about Asia-Pacific health cover

- Take the next step with BRIGENAI

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Dedicated expat cover is essential | Travel and local insurance rarely offer the full protection expats need in Asia-Pacific. |

| Choose plan features wisely | Inpatient-only often suffices but outpatient, maternity, and evacuation add-ons should be considered based on your region and needs. |

| Costs vary widely | Premiums depend on destination, age, health, and specific coverage choices—compare carefully. |

| Evaluate providers thoroughly | Review claims handling, policy flexibility, and reputation to avoid costly errors. |

Why expats need dedicated health insurance

The gap between what most expats think they have and what they actually have is where financial disasters happen. Travel insurance typically caps out at 90 days and excludes anything deemed a “pre-existing condition.” National health schemes in your home country, whether that’s Medicare in Australia or the NHS in the UK, stop covering you the moment you establish residency abroad. And local health schemes in your destination country often require permanent residency or citizenship before you can access subsidised care.

This leaves a very real coverage gap. Consider these common scenarios:

- Emergency surgery in Thailand: Private hospital bills for a serious accident can exceed AUD 80,000. Without dedicated cover, you pay out of pocket.

- Cancer diagnosis in Malaysia: Treatment costs over 12 months can reach AUD 200,000 or more. Most travel policies exclude this entirely.

- Medical evacuation from a remote area: Airlifting a patient from a regional location in Indonesia to a major city can cost AUD 30,000 to AUD 80,000 alone.

- Chronic condition management: Ongoing medication, specialist visits, and monitoring for conditions like diabetes or hypertension are rarely covered by travel policies.

“The biggest mistake expats make is assuming that because they feel healthy, they don’t need comprehensive cover. Medical emergencies don’t send a calendar invite.”

Leading providers for expats in Asia-Pacific include Cigna Global, Allianz Care, Bupa Global, Pacific Cross, ACS, and NIMBL, all offering comprehensive inpatient, cancer care, and evacuation cover with modular outpatient and maternity add-ons. These providers understand the specific risks of the region and structure their policies accordingly, which is something a generic travel insurer simply cannot match.

For expats working in APAC health roles or any other sector, the right insurance foundation is non-negotiable. The healthcare systems across Asia-Pacific vary enormously. Japan has world-class public hospitals. The Philippines has a patchwork of public and private care. Vietnam’s private hospitals in major cities are excellent, but rural care is limited. You need a policy that accounts for where you actually live, not just where you land.

Now that you know why insurance is such a critical foundation, let’s break down the main options available for expats.

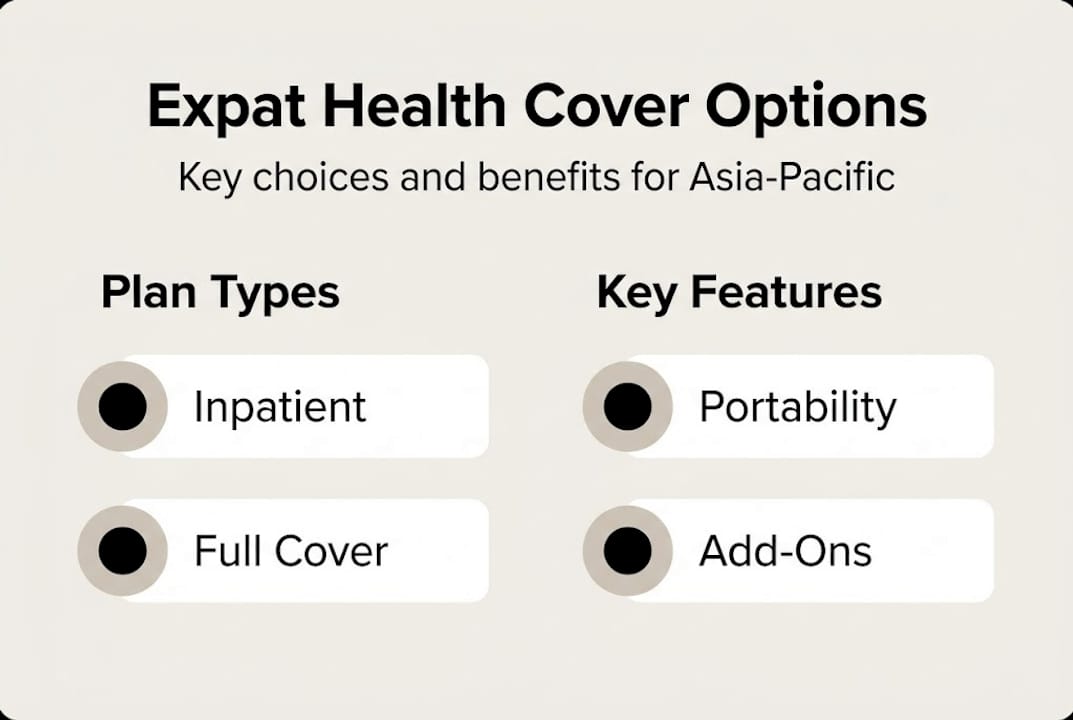

Understanding your options: Expat health insurance plans in Asia-Pacific

Not all expat health insurance is the same. The plans available to you range from basic inpatient-only cover to fully loaded international policies with every add-on imaginable. Understanding the structure helps you buy what you actually need rather than what sounds impressive.

The main plan types are:

- Inpatient-only plans: Cover hospitalisation, surgery, and emergency care. These protect you from catastrophic costs and are the minimum recommended level for any expat.

- Inpatient plus outpatient plans: Add cover for GP visits, specialist consultations, diagnostics, and prescription drugs. Useful in countries where outpatient care is expensive.

- Modular plans with add-ons: Start with a core inpatient plan and layer on evacuation, maternity, dental, vision, or mental health cover as needed.

Here’s a comparison of the main plan types to help you assess what suits your situation:

| Plan type | Best for | Key benefit | Key limitation |

|---|---|---|---|

| Inpatient only | Long-term expats, SEA residents | Low premium, catastrophic protection | No routine care cover |

| Inpatient + outpatient | Families, corporate expats | Comprehensive day-to-day cover | Higher premium |

| Modular with add-ons | Expats with specific needs | Flexible, customisable | Can become expensive quickly |

| Regional plans | Single-country or regional stays | Lower cost than global plans | Limited portability |

Portability is one of the most underrated features in expat insurance. If you’re moving between Singapore, Malaysia, and Thailand over a few years, you need a policy that travels with you. Many top-tier providers offer Asia-Pacific portability as standard, meaning your coverage doesn’t lapse or reset when you cross a border. This matters enormously for expats who change roles or countries mid-contract.

For expats in Southeast Asia specifically, community advice consistently points to inpatient cover with portability as the priority, since local outpatient costs in places like Thailand and Vietnam are genuinely affordable out of pocket, but hospitalisation bills are not. Paying for outpatient cover in a country where a GP visit costs AUD 20 is often unnecessary.

Pro Tip: Before choosing a plan, research the average cost of a private hospital night in your destination country. In Singapore, a single night in a private hospital can cost AUD 1,500 or more. In Vietnam, it might be AUD 150. That number alone should guide how much inpatient cover you need.

You can also use the AI health insurance advisor on BRIGENAI to model different scenarios based on your destination, age, and health history. And if you’re heading to New Zealand, check out the detailed breakdown of insurance options in New Zealand to understand how local and international cover interact.

With a clear picture of the main plan types, you’ll need to consider what influences cost and suitability.

Key factors affecting costs and coverage

Your premium is not just a number pulled from thin air. It reflects a combination of variables, and understanding each one helps you negotiate better terms and avoid paying for cover you don’t need.

The main cost drivers are:

- Age: Premiums rise significantly after 40 and again after 55. Locking in a policy earlier can save thousands over the long term.

- Destination country: Insuring yourself in Singapore or Japan costs more than insuring in Vietnam or the Philippines, because healthcare costs in those countries are higher.

- Pre-existing conditions: Insurers may exclude these entirely, charge a loading (a higher premium), or impose a waiting period before covering related claims.

- Coverage area: A global plan covering the US costs significantly more than an Asia-Pacific regional plan. If you’re not going to the US, exclude it.

- Add-ons selected: Maternity cover, dental, and evacuation all add to your base premium. Maternity cover in particular can add 30 to 50 per cent to your annual cost.

Here’s a rough guide to annual premium ranges for expats in Asia-Pacific in 2026:

| Profile | Inpatient only | Inpatient + outpatient | Full cover with add-ons |

|---|---|---|---|

| Single, age 30, SEA | AUD 1,200 to 2,000 | AUD 2,500 to 4,000 | AUD 4,500 to 7,000 |

| Single, age 45, Singapore | AUD 2,500 to 4,000 | AUD 4,500 to 7,000 | AUD 8,000 to 12,000 |

| Family of 4, SEA | AUD 5,000 to 8,000 | AUD 9,000 to 14,000 | AUD 15,000 to 22,000 |

These are indicative ranges only. Actual premiums depend on your specific health history and the insurer’s underwriting approach. The cost of living in Singapore is a useful reference point when budgeting for healthcare costs alongside rent, transport, and daily expenses.

Experts consistently recommend inpatient cover plus portability for Southeast Asia, given that hospitalisation costs are the real financial risk, while routine outpatient care remains relatively affordable in most of the region.

Pro Tip: In Southeast Asia, consider skipping outpatient cover and instead budgeting AUD 50 to AUD 100 per month for out-of-pocket GP visits. Redirect those savings to a higher inpatient limit or add evacuation cover instead.

Once you understand costs and benefits, you’ll want to know how to actually select the right provider and compare your options.

How to compare and choose the best provider

Choosing an insurer is not just about finding the cheapest quote. The claims process, customer support quality, and policy exclusions matter just as much as the premium. Here’s a structured approach to making the right call.

- Assess your actual needs. Where are you living? Do you have dependants? Any pre-existing conditions? Are you planning to have children? These answers narrow your options immediately.

- Shortlist three to five providers. Focus on those with a strong presence in your destination country. Reputable providers like Cigna Global, Allianz Care, Bupa Global, Pacific Cross, ACS, and NIMBL are well-established in Asia-Pacific and have proven claims track records.

- Request quotes and compare like for like. Make sure you’re comparing the same benefit limits, deductibles, and coverage areas. A lower premium often means a higher excess or lower annual limit.

- Read the exclusions carefully. This is where most expats get caught out. Look specifically for exclusions around pre-existing conditions, mental health, adventure sports, and cross-border care. Some policies exclude care in your home country entirely.

- Check claims reputation. Search expat forums and community groups for real experiences with your shortlisted providers. A provider with a smooth, fast claims process is worth paying a small premium for.

- Verify the network hospitals. Confirm that your preferred private hospitals in your destination city are on the provider’s direct billing network. Direct billing means you don’t pay upfront and claim back later, which matters enormously during a stressful medical event.

Pro Tip: Use a specialist expat insurance broker rather than going direct to the insurer. Brokers who work exclusively with international clients often have access to better rates, can negotiate exclusion waivers for pre-existing conditions, and will advocate for you during a disputed claim.

You can run initial comparisons with smart expat tools on BRIGENAI to get a structured starting point before you engage a broker or insurer directly.

A fresh take: What most expats miss about Asia-Pacific health cover

Here’s what years of watching expats navigate this region has taught us: most people either over-buy or under-buy their health cover, and both mistakes are driven by the same thing. Fear or overconfidence, not actual analysis.

New arrivals often buy the most expensive “deluxe” plan because it feels safe. But a 28-year-old in good health living in Chiang Mai does not need the same policy as a 52-year-old with a family in Singapore. Buying more than you need is money that could go toward building an emergency fund or investing in your career.

On the other side, experienced expats who’ve been in the region for years sometimes drop their cover entirely, convinced they know the system. That’s when things go wrong. A single serious illness or accident can undo years of financial progress.

The insider truth is that local advice often lags behind global realities. A colleague who’s been in Bangkok for five years might swear their local Thai insurer is fine, but that policy may not cover them in Malaysia, may exclude conditions that developed since they took it out, and may have a claims process that falls apart under pressure.

Flexible, modular policies reviewed annually are almost always better than locked-in “comprehensive” plans that you set and forget. Your needs at 30 in Kuala Lumpur are not your needs at 40 in Tokyo. Review your policy every time your life changes, and compare the market every two to three years. That discipline alone can save you thousands and ensure you’re never caught without the cover you actually need.

Take the next step with BRIGENAI

Navigating health insurance as an expat is genuinely complex, and the stakes are high. BRIGENAI exists to make that process clearer and faster.

Whether you’re comparing destinations, planning your relocation, or trying to understand what cover you actually need, BRIGENAI’s tools and advisors have you covered. Explore our relocation services to get structured support from people who’ve made the same move. Use our immigration support AI to navigate visa requirements alongside your health planning. And browse our visa guides to understand how residency status affects your insurance eligibility in each destination country. Your next move deserves better than guesswork.

Frequently asked questions

Do I need international health insurance if I already have travel insurance?

Travel insurance usually only covers short-term emergencies and doesn’t provide comprehensive, ongoing healthcare abroad. For expats, dedicated international cover is essential from day one.

What is the most important cover to include in my expat health policy?

Inpatient and hospitalisation cover is essential to protect against costly medical emergencies. As experts advise, inpatient-only plans handle the catastrophic costs that can genuinely ruin you financially.

Is maternity or dental cover standard in expat health plans?

Maternity and dental are usually optional modules that increase your policy cost. Leading providers offer these as add-ons rather than standard inclusions in base plans.

Will my expat health insurance cover me in different countries if I relocate within Asia-Pacific?

Many top providers offer portable plans that keep you covered as you move across countries in the region. Portability is strongly advised for expats in Southeast Asia given the frequency of cross-border movement.